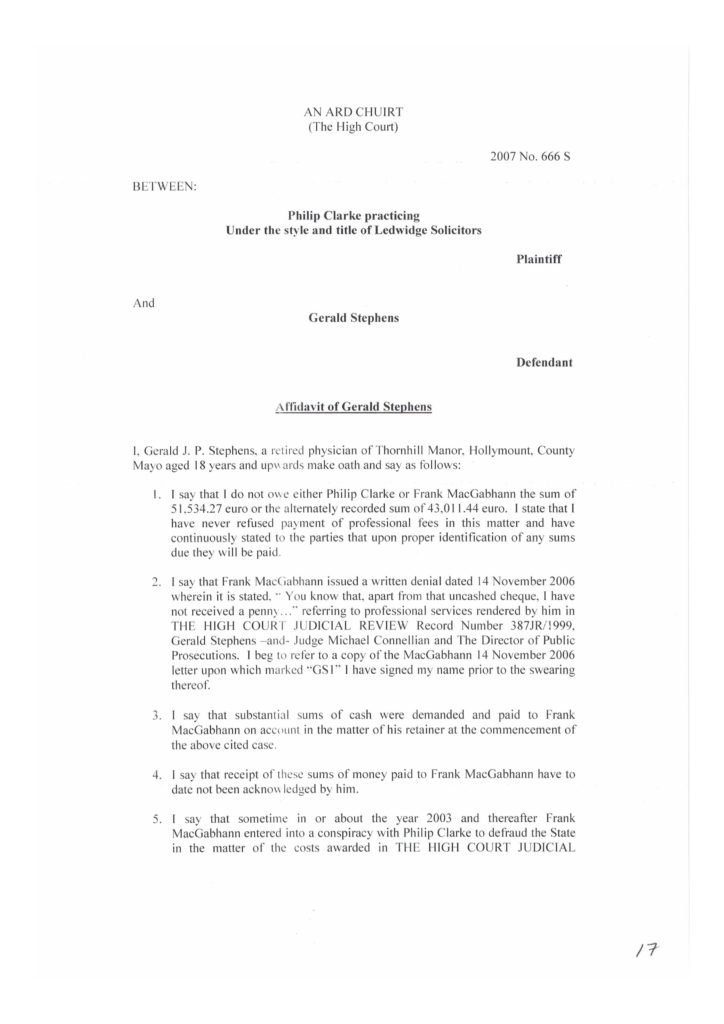

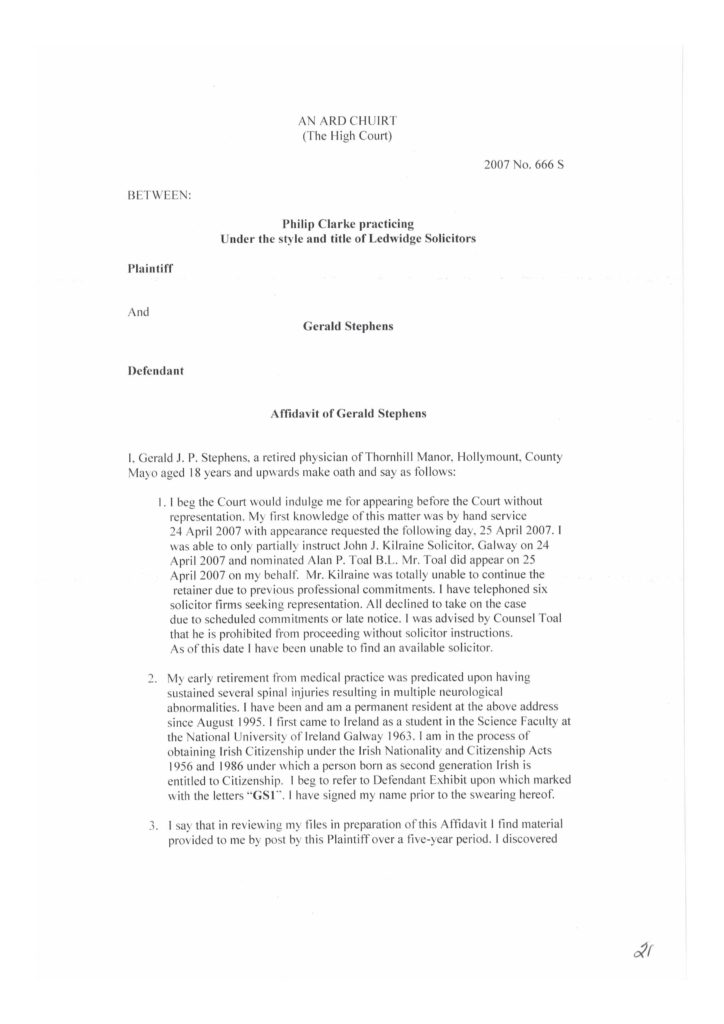

Supreme Court Aborts Hearing Allegations of Prejudgment Bias and Misprision – Court conducts hearing, judgment and order in absentia

The predicate for the allegations arose when the current Supreme Court Chief Justice sat at hearing of the High Court in Philip Clarke practicing under the style and title of Ledwidge Solicitors and Gerald J. P. Stephens, High Court 2007 No. 666S.

History

High Court Record No. 1999 387JR in the matter of Gerald Stephens v Judge Michael Connellan and the Director of Public Prosecutions shows that the charges against Gerald Stephens, Firearms Act, the illegal importation of firearms and ammunition were set aside by Mr. Justice McKechnie in a 52page Judgement given on 21 December 2001. The Court further ordered costs to Stephens.[1]

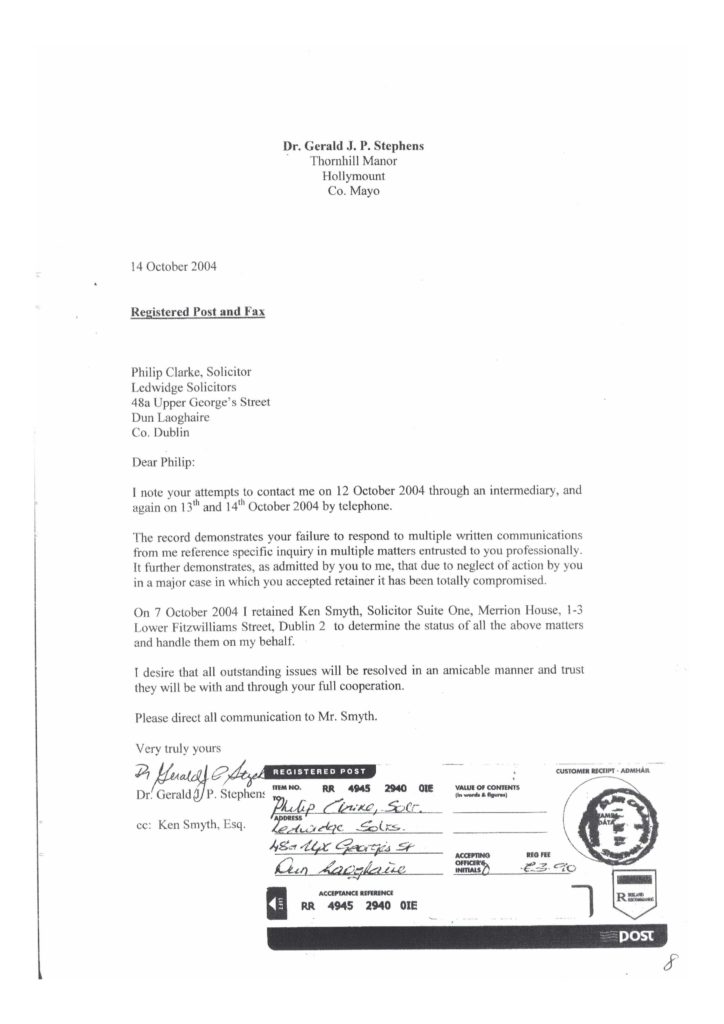

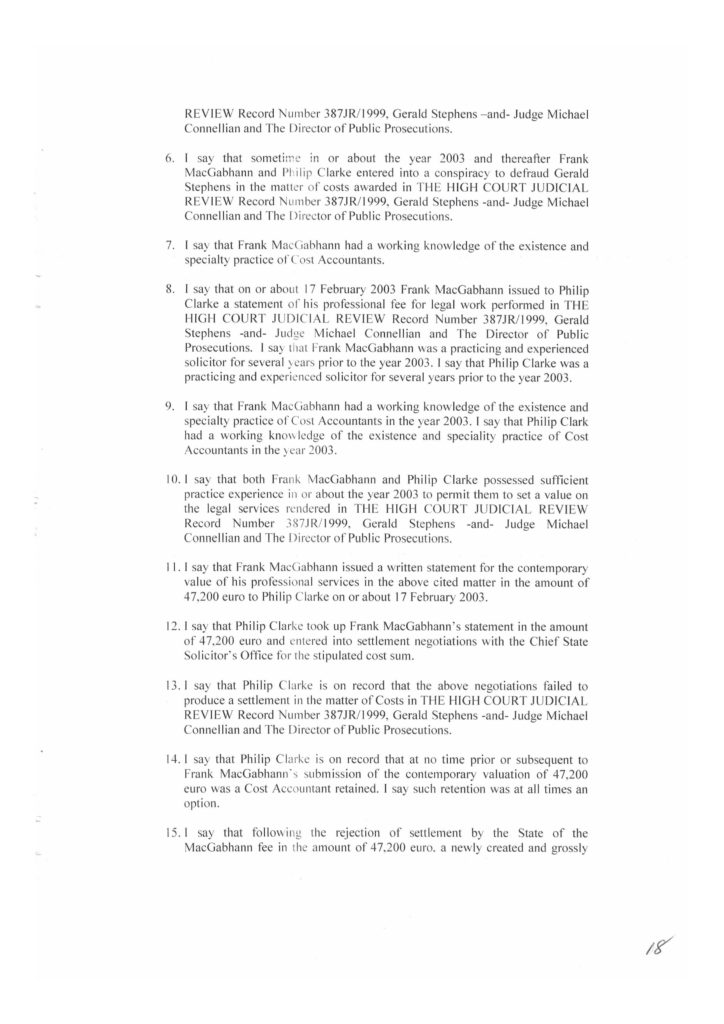

Following the above, the solicitor acting for Stephens withdrew from private law practice to take up a position with the State. He referred Stephens to Philip Clarke, a solicitor for the purpose of executing collection of the ordered costs. Solicitor Clarke obtained, with the file, the original fee statements submitted by all the retained legal representatives. However, he failed, refused or neglected to take any further action in the matter for the period of c.3 years.

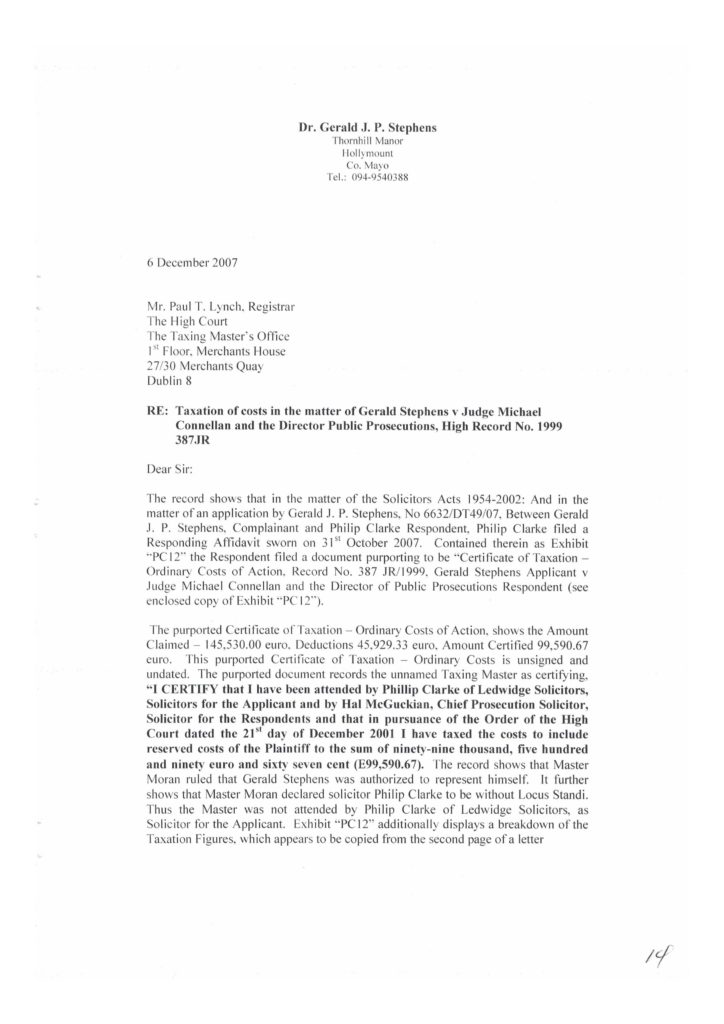

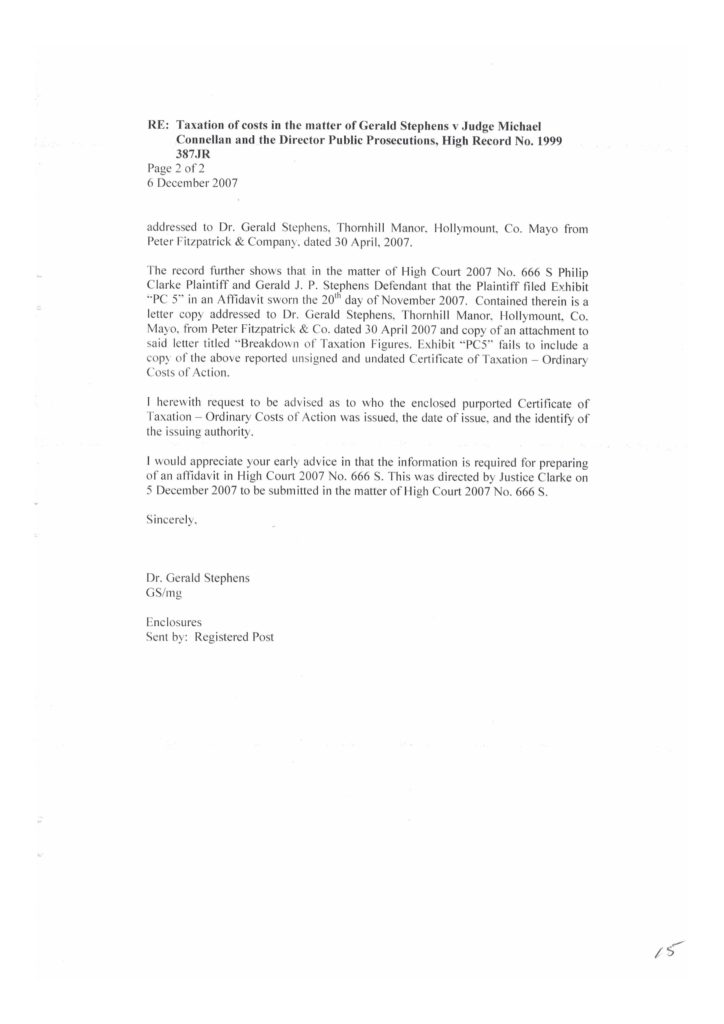

Mr. Clarke’s retainer was terminated in 2004 for cause in the above and failure to prosecute a libel case under his retainer which resulted in dismissal of the matter. Subsequent to the registered post notice of termination, solicitor Clarke listing himself as solicitor of record acted without authority in 2007 on his former client’s behalf where he filed Notice of Taxation before the Tax Court in the Judicial Review Order for costs. At hearing of the matter, the Master ruled that solicitor Clarke did not represent Gerald Stephens and permitted the latter to proceed pro se.

The Tax Court issued an order in the amount of 99,590.67 euro for costs against the State. The order further directed that the proceeds be paid only in the name of Gerald Stephens. Solicitor Clarke immediately filed a High Court Summary action against Stephens, Philip Clarke practicing under the style and title of Ledwidge Solicitors and Gerald J. P. Stephens, High Court 2007 No. 666S.

The action was commenced without consultation or determination with Stephens reference settlement of outstanding legal fees. The matter was listed for hearing before the High Court Master.

Clarke, through Counsel Rutherdale, presented to the court that a Certificate of Taxation was issued by the Tax Court and the ground for the Summary action. Defendant Stephens stated to the Court that no Certificate of Taxation was issued by the Tax Court. The Master ordered the matter to proceed before the High Court. The case was eventually listed to be heard by Mr. Justice Frank Clarke.

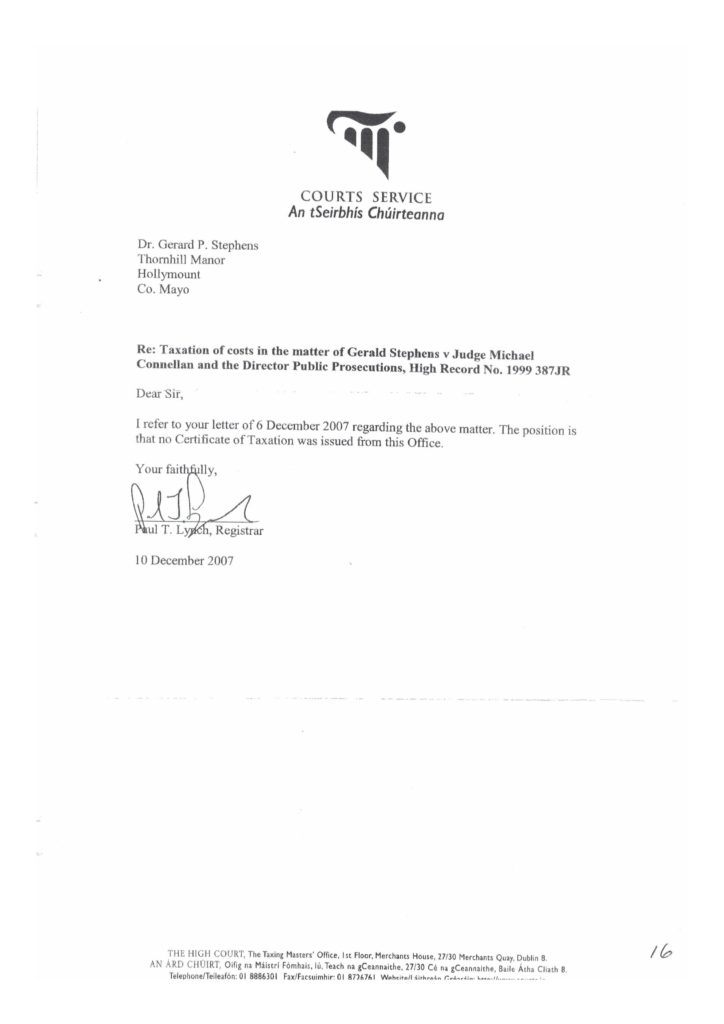

The issue of the non-existence of a Certificate of Taxation issued by the Tax Court was opened by Stephens. Mr. Justice Clarke on 5 December 2007 adjourned the hearing with order to Stephens to produce evidence of the allegation that no Certificate was ever issued by the Tax Court with comment that this was a very serious allegation that would “change the entire matter”. The evidence was obtained within five days (5) days and submitted to the court by affidavit.

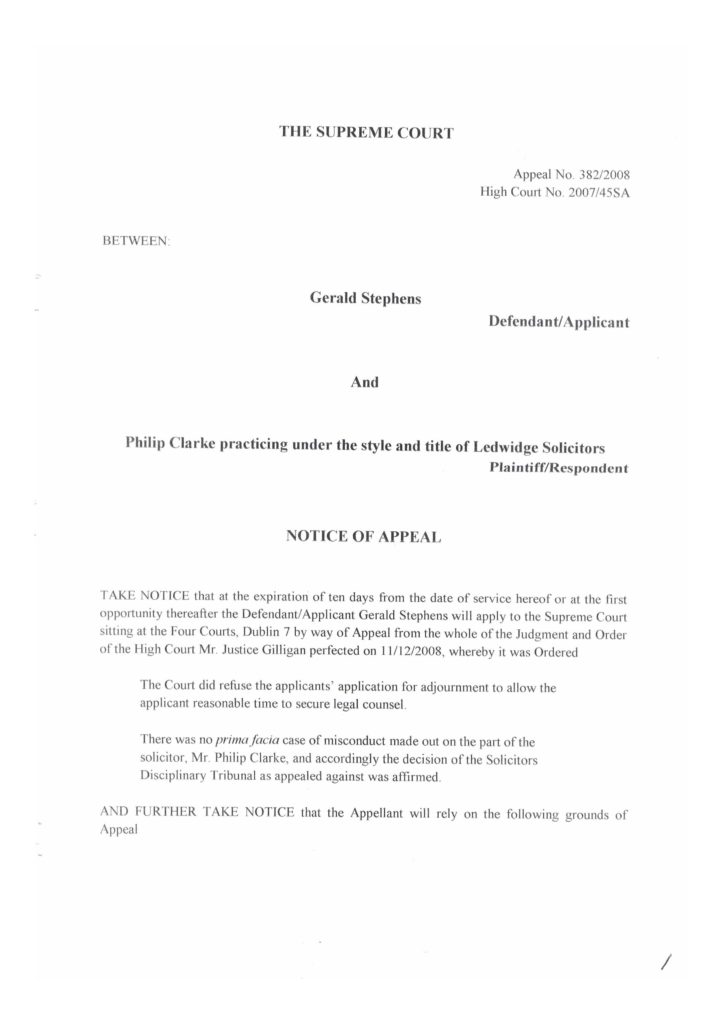

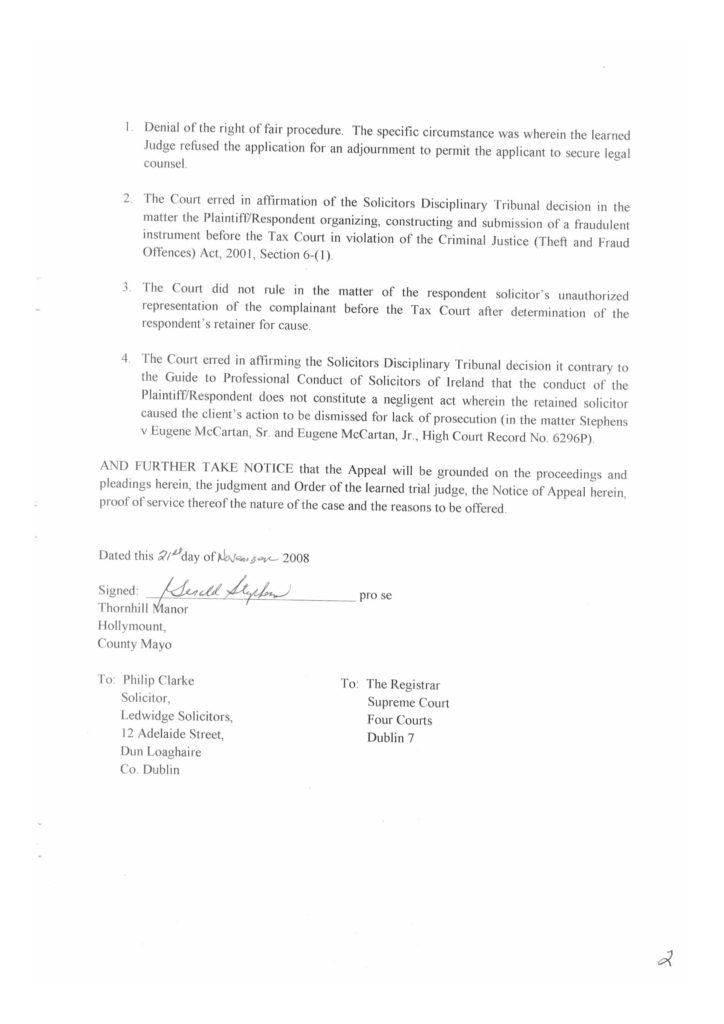

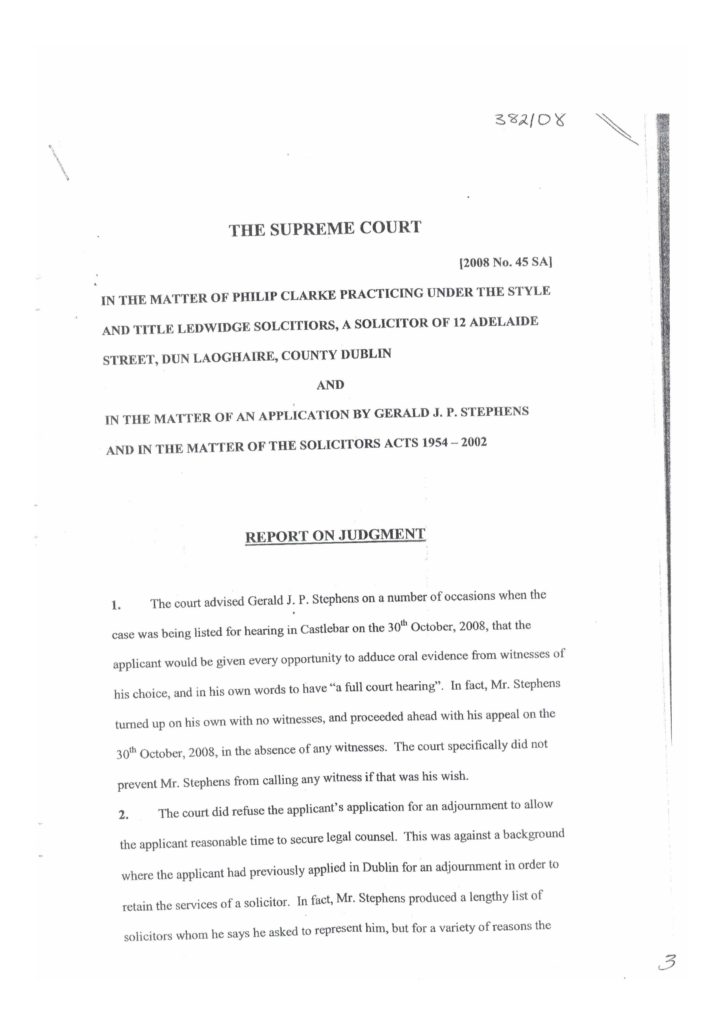

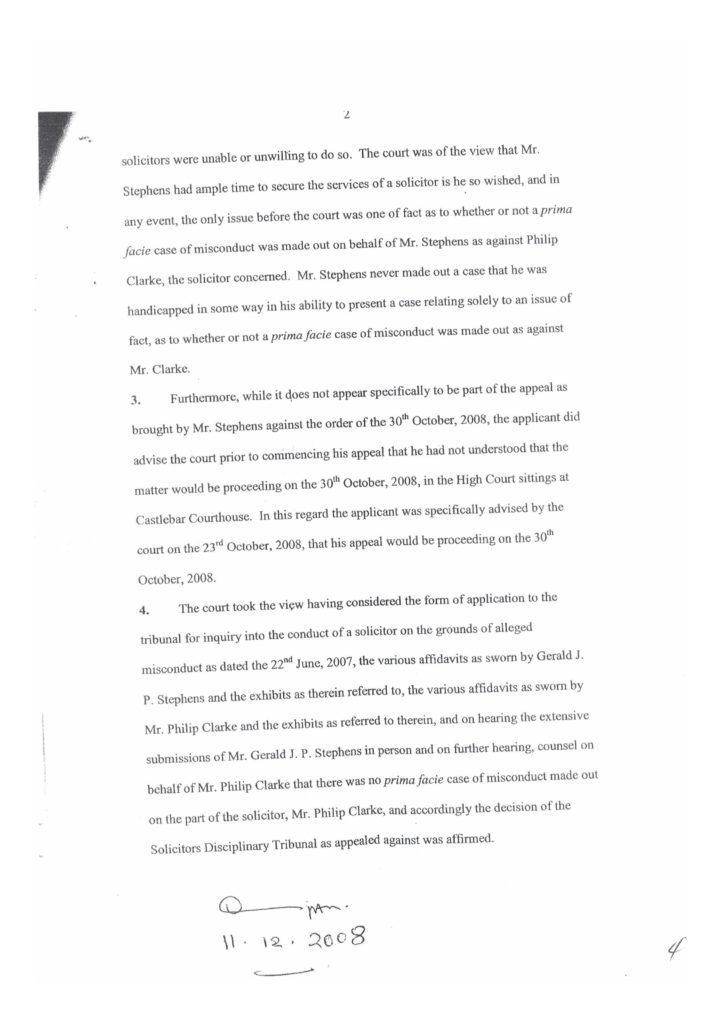

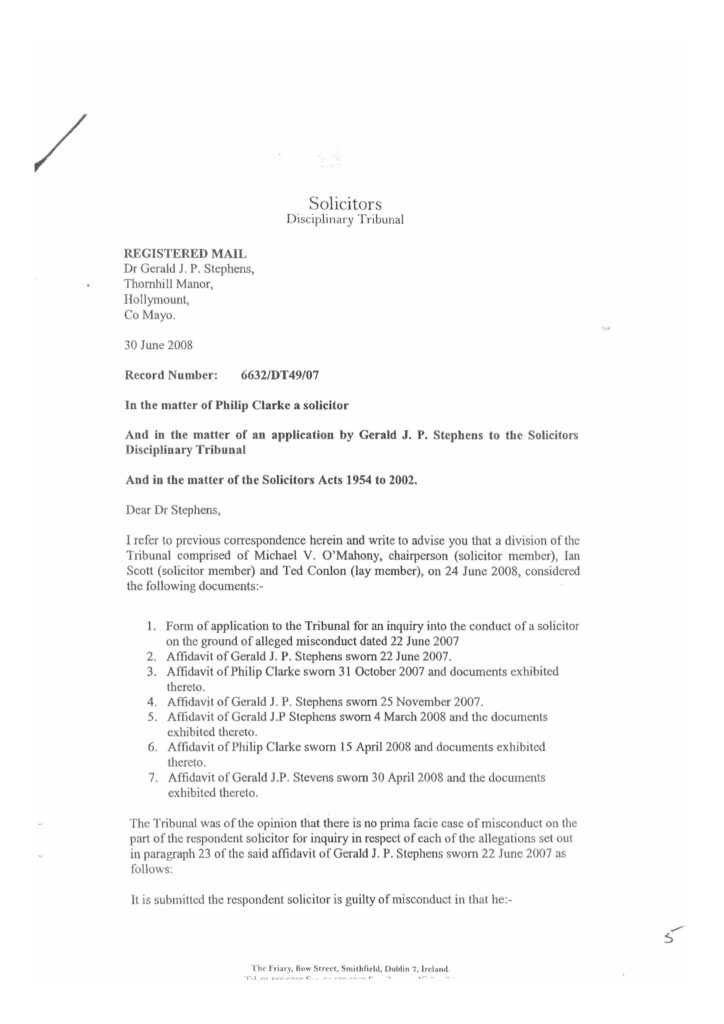

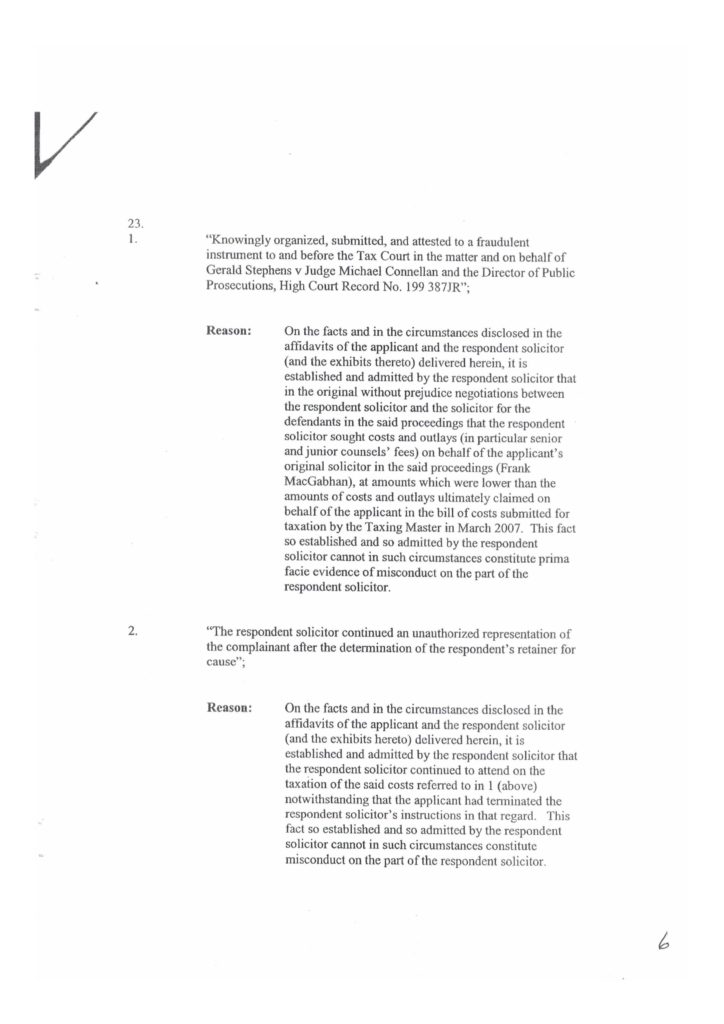

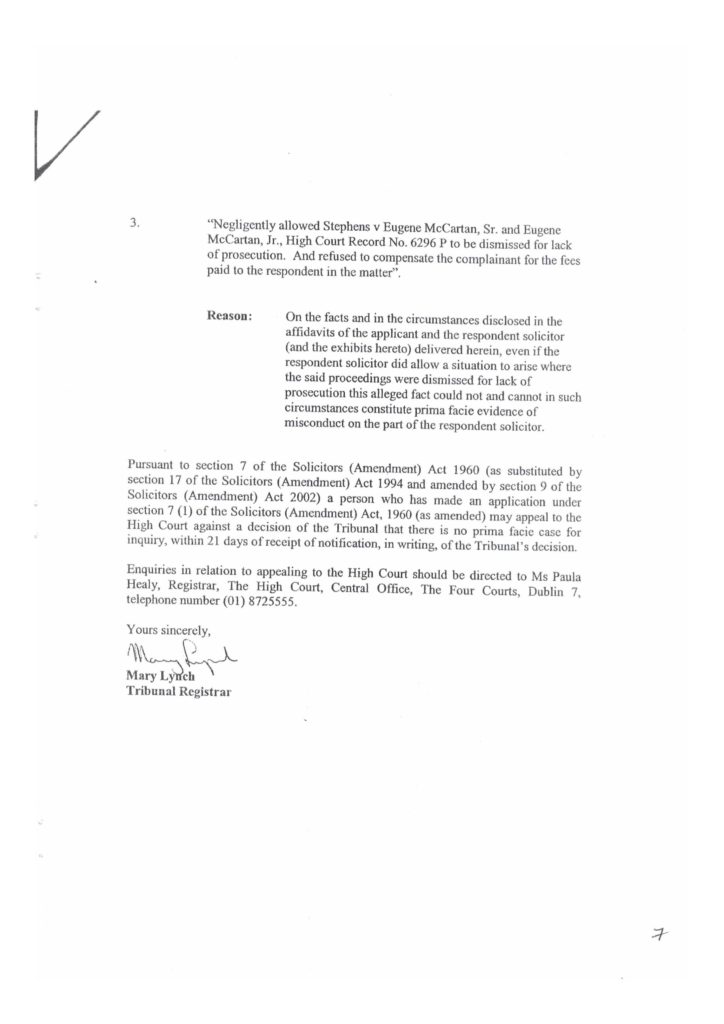

Stephens’ letter of 6 December 2007 to Paul T. Lynch, The High Court, Registrar, The Taxing Masters Office and Registrar Lynch’s response of 10 December 2007 are seen below in an affidavit before the Supreme Court Appeal No.382/2008, High Court No.2007/45SA. The latter case was predicated on appeal to the President of the High Court of the Solicitors Disciplinary Tribunal record No 6632/DT49/07 ruling against Stephens in his complaint to that body in the matter of Philip Clarke, Solicitor. The President, Mr. Justice Johnson ordered the matter to be heard in full hearing, not on affidavit.

The hearing was presided over by High Court Gilligan J who forced the matter to be heard on ‘affidavit’. That decision also appearing in the affidavit referred to above. Multiple other matters involving this Judge are presented in future posts.

At the conclusion of the hearing portion of High Court No. 2007/666S Mr. Justice Clarke opened an opportunity for the litigants to make closing statements before giving judgement. Defendant Stephens stated that the conduct exhibited by Mr. Clarke, a solicitor, throughout the entire matter represented scamming the system and was illegal. Justice Clarke, in a reported and recorded outburst said, “You are the one scamming the system and you did it in the other case.” He then proceeded to give Judgment against the Defendant.

Issues at Appeal before the Supreme Court hearing in absentia with dismissal stipulation designed to never allow the matter to be heard and recorded. Pre-judgment Bias against the Defendant.

- Plaintiff’s action after his retainer was withdrawn for cause in filing a Claim before the Tax Court on behalf of the former client in the matter of High Court No. 1999 387 JR.

- Plaintiff conspiring with other members of the bar to create and file fraudulent statements of legal fees.

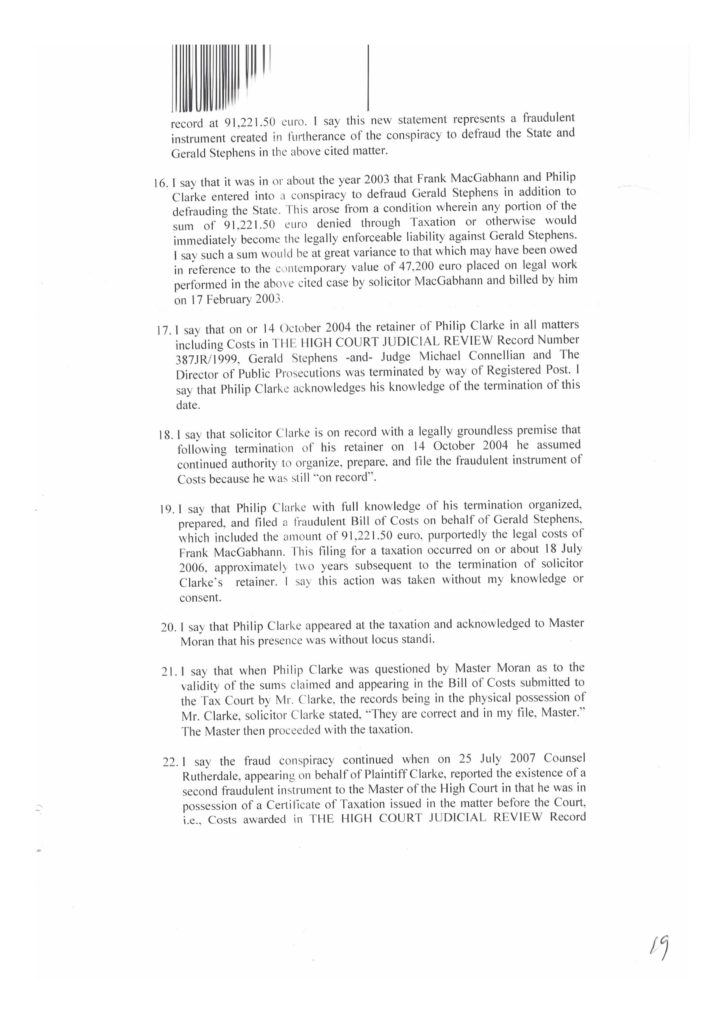

- Plaintiff’s conduct in filing a fraudulent statement of fees on behalf of the co-conspirators before the Tax Court.

- Plaintiff conduct in in filing a false Affidavit in the matter of an alleged Certificate of Taxation.

[1] Editor’s Note: High Court Mr. Justice William M. McKechnie, High Court No. 1999 387 JR Decision appears at courts.ie. The record reveals the genesis of matters involving Dr. Gerald J. P. Stephens following retirement in Ireland.

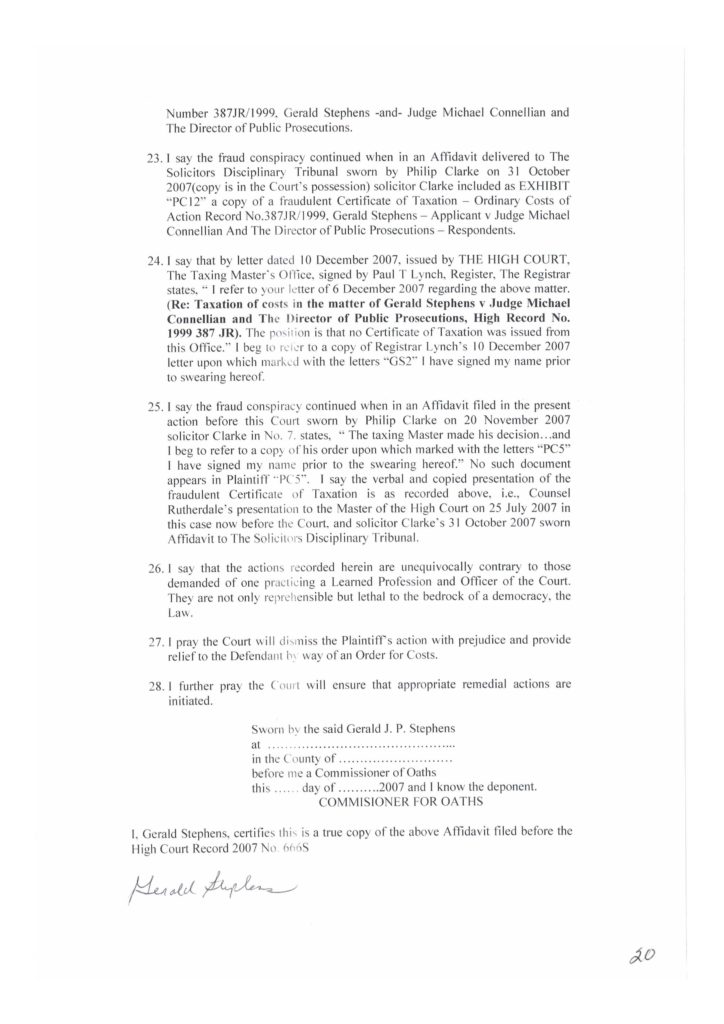

N.B. Follow up for the next ICW post will continue to provide further documentation in all matters opened in previous posts.